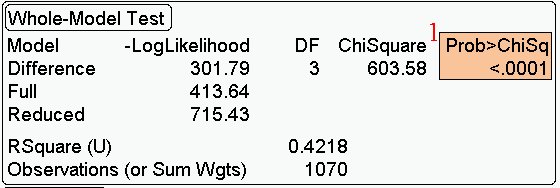

1. The overall test in logistic regression. Is anything going

on, are any (any combination) of the predictors useful in

predicting Y (the logits of the probabilities)? In this case the

small p-value indicates that this

is the case.

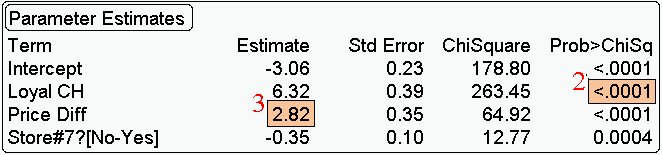

2. Is a specific coefficient significant (useful) after having

controlled for the other variables in the model. The small p-value

says this is indeed the case.

3. What does the 2.82 tell you?

For every 1 unit change in price diff the logit of the probability

of buying CH changes by 2.82. (controlling for loyal ch and store 7.)

BETTER. For every one unit (ie a dollar) change in

price diff the

odds of buying CH changes by a multiplicative factor of exp(2.82)

= 16.8.

Key calculation. At Loyal CH of 0.8, price diff of 20 cents

and product sold in store 7, predict the probability of buying CH?